Market Opportunities

Armory was founded to take advantage of the team’s extensive expertise in advising and investing in middle market companies over the past 30 years. As the capital markets have expanded, middle market companies have increasingly experienced a lack of access to capital, creating market inefficiencies that Armory believes it can exploit due to our comprehensive capabilities in working with middle market companies.

WHY THE MIDDLE MARKET

By “middle market,” Armory targets companies with EBITDA ranging from $10 million to $100 million, generally with less than $1 billion of debt outstanding and issue sizes ranging from $200 million to $500 million. Opportunities in the middle market may result from pockets of weakness in the U.S. economy, company specific issues, or industry specific issues. Over the past eight years, growth in the capital markets has been focused predominantly on larger companies with greater trading liquidity. Consequently, we believe this has resulted in significant inefficiencies in the middle market, which has and continues to generate substantial investment opportunities.

There are three core reasons why Armory focuses on the middle market:

-

1. Armory believes there are more inefficiencies on which to capitalize in the middle market because most traditional credit funds, as well as credit hedge funds, focus on larger cap companies in order to deploy larger amounts of capital than possible in the middle market. This leads to thin coverage of middle market companies by Wall Street, providing a potential advantage for Armory's team who has experience sourcing and investing in this part of the market. Additionally, when high yield funds and collateralized debt funds hold middle market debt in their portfolios, they will tend to sell these issuers first to reduce liquidity risk in their portfolio, creating an attractive supply/demand imbalance.

2. Armory believes its ability to source companies in the middle market is substantially better than for larger companies due to greater market access provided by relationships the team has formed over the past 30 years.

3. In situations which may require a restructuring, Armory believes there is a greater opportunity to have significant control over the process in middle market companies because other investors in these situations are usually par buyers who have little if any experience in restructuring companies and are looking for guidance. Additionally, the Armory platform provides access to unique investment opportunities and substantial resources for a successful restructuring.

ARMORY PLATFORM

Founding partners Nick Tell and Eben Perison formed Armory Group to create a unique platform focused exclusively on middle market companies. In addition to asset management, Armory’s middle market platform consists of investment banking and consulting services. The chart below briefly describes the focus of each of Armory’s entities and the market segment that each targets.

The Armory Group team has over 200+ collective years of broad and diverse experience in credit, legal and financial restructurings as well as investing, consulting and investment banking. In addition, Armory has 12 industry verticals via Armory's investment banking group, providing further resources to Armory's investment team.

Armory believes this platform provides Armory investment team unique access to investment opportunities and diligence resources in four ways:

-

1. Knowledge sharing across the platform facilities a deeper bench of industry expertise and real-time insights into current market dynamics for middle market companies;

2. Broader access to relationships with key constituents in the stressed/distressed arena provides resources and access to investment opportunities from longstanding relationships across the platform;

3. Deep relationships with over 400 direct lending funds from investment banking team’s focus on raising capital for middle market companies provides Armory's investment team access to potential distressed opportunities in the direct lending sector.

4. Consulting and strategic advisory capabilities provides resources to the investment team in assessing and implementing turnaround plans in portfolio companies at no additional costs to investors or portfolio companies.

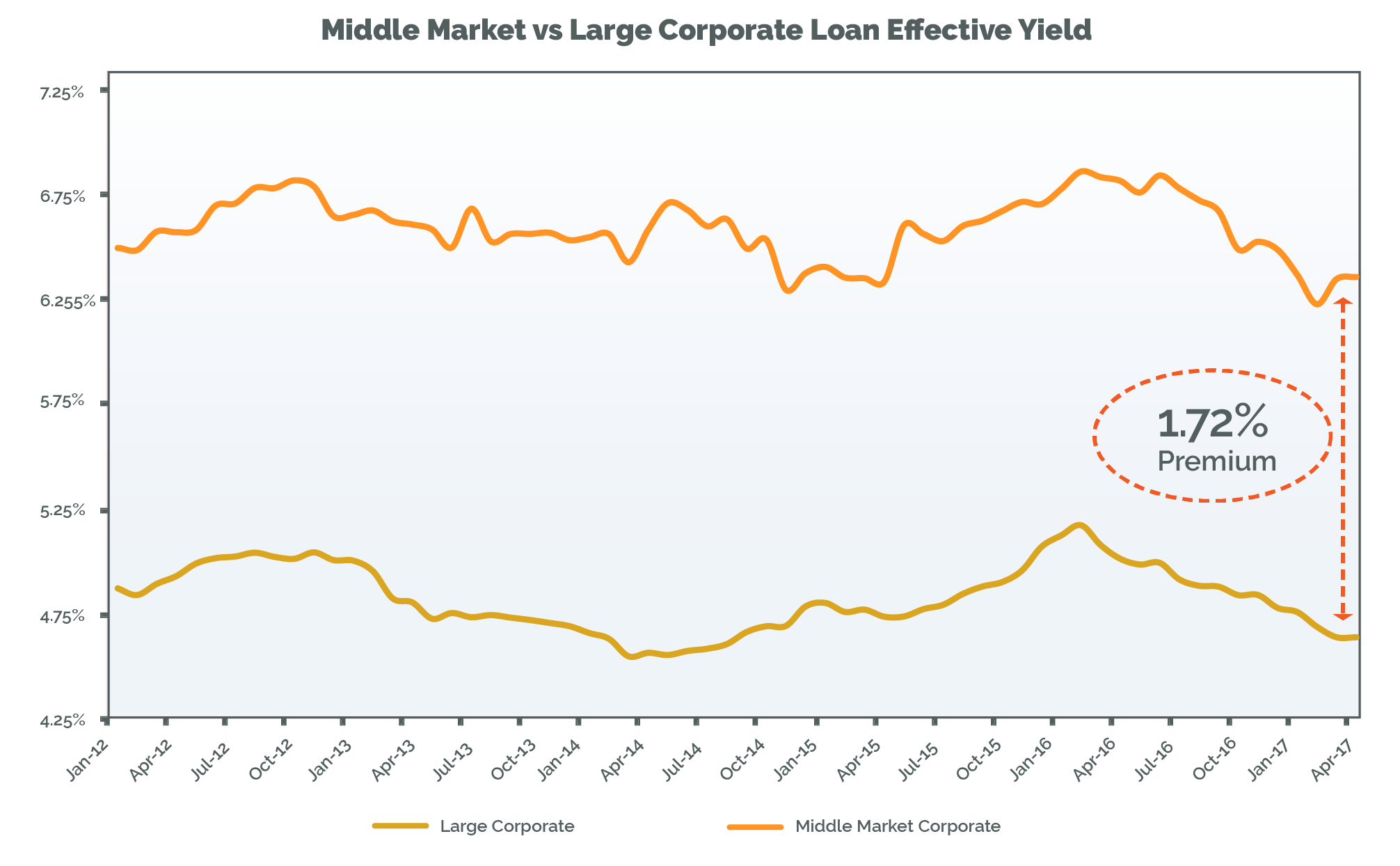

OPPORTUNITY IN MIDDLE MARKET BANK DEBT

Armory focuses on investing in a portfolio of leveraged loans with issue sizes generally ranging from $200 million to $500 million for three reasons Armory believes are unique to small issue size syndicated leveraged loans:

-

1. Better access to management and better covenants than large, broadly syndicated loans.

2. Higher liquidity than smaller, direct lending club loans because agent banks for small issue size leveraged loans are typically the same agent banks as for the large, broadly syndicated loan market and typically provide daily markets for these loans.

3. Consistent yield premium over large, broadly syndicated loans even at times of market volatility in the leveraged loan market. See chart below for historical spread premiums.

*Source: Standard & Poor's

OPPORTUNITY IN

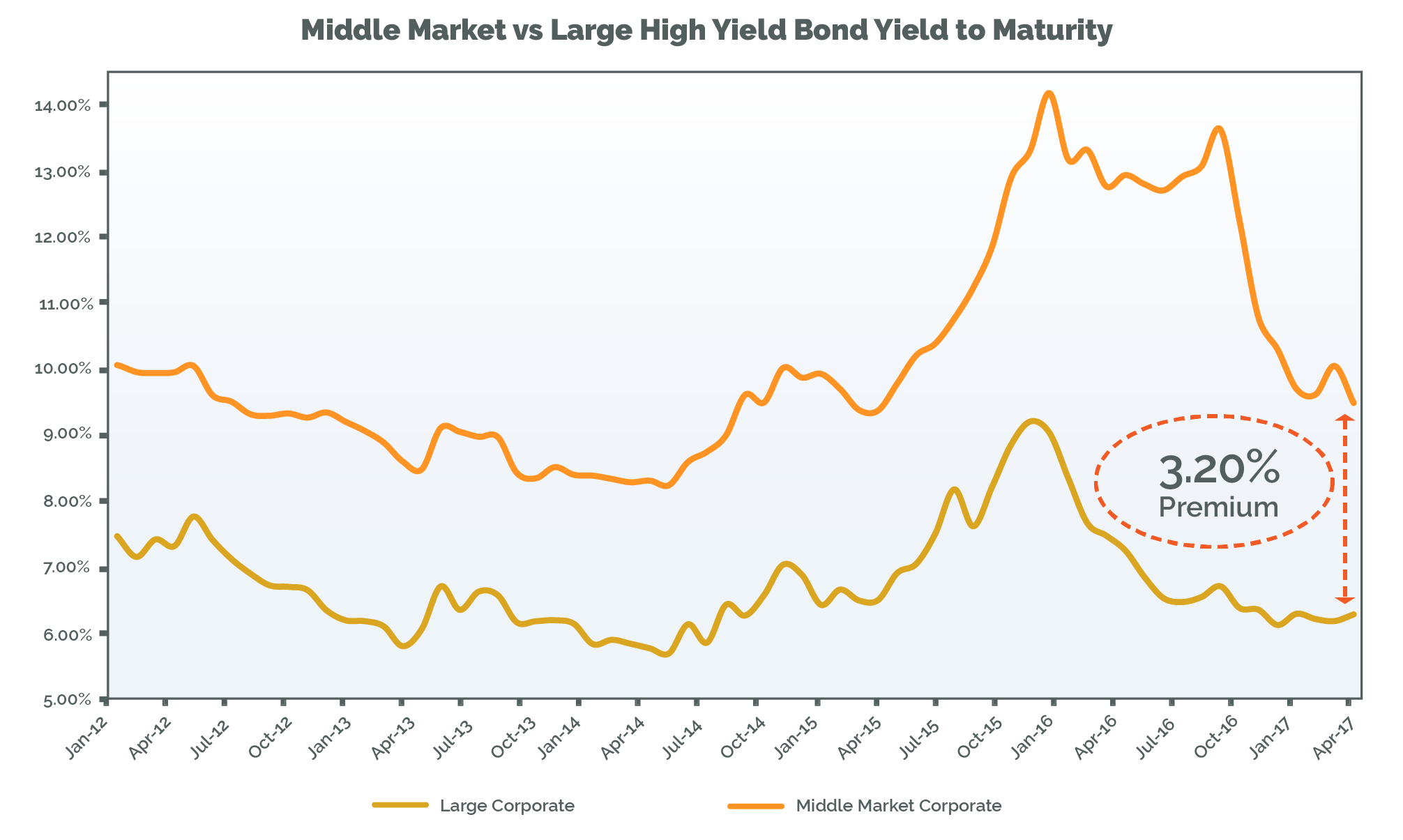

HIGH YIELD

Armory has focused on investing in high yield bonds with issue sizes generally ranging from $200 million to $500 million because there is a significant yield premium over the large issue size high yield market. This yield premium has widened significantly over the past 10 years as Exchange Traded Funds (ETFs) started dominating the overall high yield market. ETFs cannot typically invest in these small issue high yield bonds due to the ETFs liquidity requirements.

As shown in the chart below, the yield premium for these small issue size high bonds widens substantially during times of market volatilty in the overall high yield market. As a result, Armory believes the best environment to invest in these small issue size high yield bonds are during periods of volatility in the overall high yield market.

*Source: JP Morgan

During times of low volatility, Armory is positioned to take advantage of market volatility when it happens with a list of 15 to 20 issuers which were previously owned by Armory’s funds but were sold as the market tightened.

OPPORTUNITY IN DISTRESSED

Maturity Wall for Small Issue High Yield

Armory’s distressed strategy over the past five years has focused on small issue size high yield bonds with short dated maturity dates. The supply of these short-dated maturities continues to grow as approximately 60 percent of high yield issues with 2020 or earlier maturities are small issue size high yield bonds. This growing “maturity wall” has created significant opportunities in middle market distressed companies for two reasons:

-

1. Capital market dynamics, industry challenges or company specific issues all negatively impact a debtor’s ability to refinance their debt at maturity, requiring these companies to restructure.

2. Middle market companies with 2020 or earlier maturities will need to address their capital structures at least one year in advance of their maturity date due to concerns over receiving “going concern” opinions on their financial statements.

*Source: Bloomberg

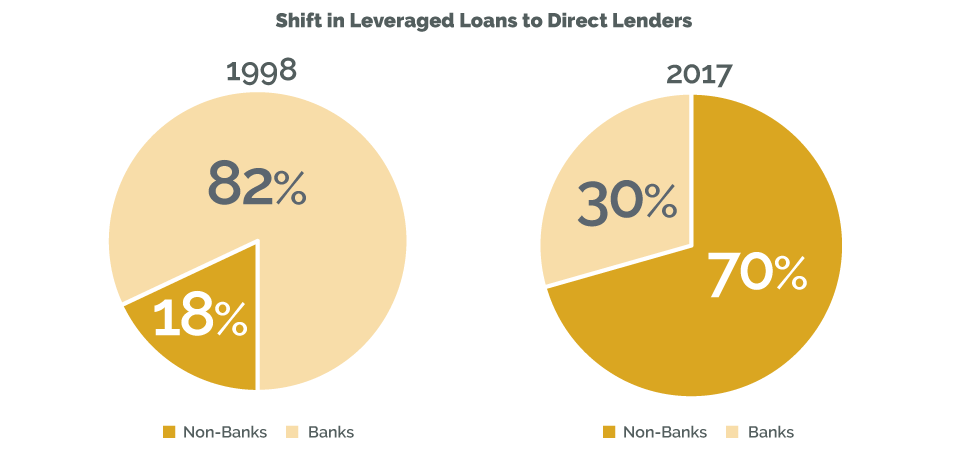

OPPORTUNITY IN DISTRESSED - GROWTH OF PRIVATE DEBT FUNDS

The growth of direct lending funds has increased exponentially over the past 5 years as the high yield market has been effectively shut for small issue size yield because ETFs are not typically able to invest in small issue size high yield. In addition, the other traditional source of financing for middle market companies, regional banks, has also reduced lending to small companies due to increased regulatory requirements as shown by the charts below.

*Source: Standard & Poor's

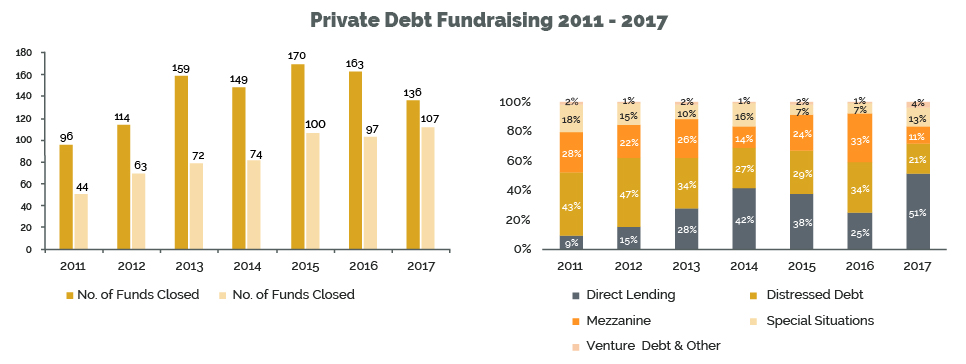

As a result, annual private debt fundraising saw continued growth in 2017, reaching over $100 billion for the first time. See table.

*Source: Preqin

Armory believes this explosive growth in direct lending over the past 5 years will create increased distressed opportunities as underwriting standards have begun to deteriorate, which will become more evident as the economy begins to slowdown over the next few years. Most of these direct lending funds do not have the expertise or resources to effectively restructure troubled loans in their portfolio. As a result, Armory expects that many of these funds will likely look to sell their troubled loans. Armory believes that it is uniquely positioned to take advantage of these opportunities due to Armory’s relationships with over 400 direct lending funds through its investment banking and advisory platform.